Is BankID ready - or able - to adjust to what’s coming?

Plus: It’s time for digital trust to be as hyped as AI itself

Hi everyone, thanks for coming back to Customer Futures.

Each week I unpack the disruptive shifts around Empowerment Tech. AI Agents, digital wallets, Personal AI in and the future of the digital customer relationship.

If you haven’t yet signed up, why not subscribe:

Hi folks,

Three simple stories, and three simple takes for you this week:

It’s time for digital trust to be as hyped as AI itself

Is BankID ready - or able - to adjust to what’s coming?

AI Agents are going to need their own identity and their own money

… and much more

It’s never been more important to understand the future of the digital customer.

So welcome back to the Customer Futures newsletter.

Let’s Go.

It’s time for digital trust to be as hyped as AI itself

It’s weird to say that AI is both over-hyped, and yet under-hyped at the same time.

Why?

Because at the lower levels of the AI stack, the market is already wide open. RAG frameworks, foundation models and GenAI platforms are rapidly becoming commodities.

Open-source alternatives (especially from China), now compete with many of the industry’s best proprietary models (especially from the US).

And at that level of AI, the market is starting to look like a utility, rather than a differentiated software category.

Sam Altman already thinks that LLM-based intelligence will become so widespread, so cheap and so part of everyday life that AI will eventually be as common as electricity.

And that’s the snag.

Can the AI Majors really sustain - and recover - the $800bn of annual investment in a market where the main products are trending to free?

Over-hyped.

But higher up the AI stack, ‘above the waterline’ towards AI agent systems and personal agents, it feels like things are under-hyped.

I don’t mean that there aren’t frothy predictions about the $Tn market about to be ‘unleashed’. Or that AI agents won’t be freely available and embedded into pretty much everything.

It’s because we simply have little idea what happens once Personal AI agents start to act on behalf of people at scale. How disruptive they will be to today’s customer experiences, customer relationships, and to every company’s digital and data processes.

And not just for AI payments (all the ‘Agentic Commerce’ stuff). But all the rest of your customer interactions.

From bookings, upgrades, account management and onboarding, to complaints, product discovery, loyalty and customer services. And so much more.

Under-hyped.

And yet what’s the barrier to all that value being created?

Digital trust.

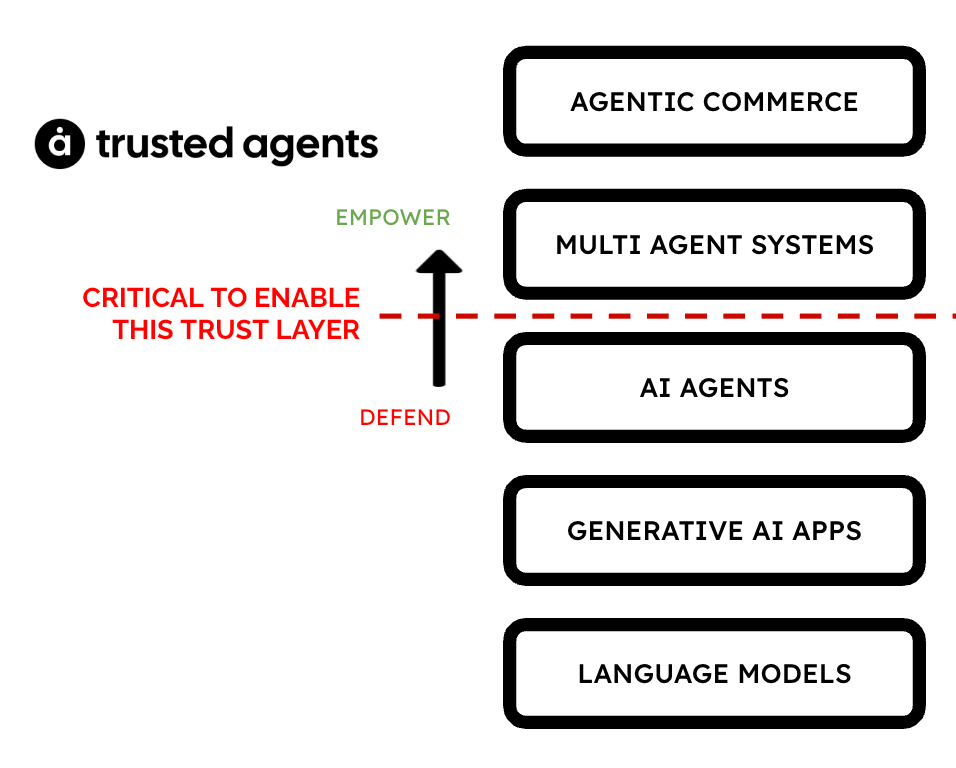

Here’s the picture we use at Trusted Agents to explain what we mean.

Yes, trust means security, privacy, audit and governance. But it also needs to include new trusted commercial models, new delegated user experiences, and new levels of data transparency and control.

Trust is going to be critical to AI Agents taking off. To scaling across the economy. And it’s precisely why Gam and I set up Trusted Agents in the first place.

Anyway, it’s one of the reasons I pay attention to things like Experian announcing ‘Agent Trust’. And not just their announcement. But their partnership with Skyfire (leading on ‘Know Your Agent’ trust) and Cloudflare (leading on internet network trust).

Quite a global combo of capabilities.

From the announcement:

Skyfire’s KYA protocol issues signed JWTs with verified identity and payment claims for each agent

Experian’s Human-to-Agent Binding enriches those claims against its consumer identity data and issues a real-time trust score

Cloudflare validates the trust signals at the network edge, before requests reach the merchant’s origin

They are bang on-trend, of course.

Because every identity, wallet and trust company has now pivoted to being an agent-identity company, an agent-wallet company, and an agent-trust company.

Quite sensibly. ‘Skate to where the puck is going’ etc. And now the market is heating up, it’s going to be a real zoo of new customer capabilities.

Some things will fly, some will swim, and some will walk.

From on-device Personal AI and agent registries, to agentic identity wallets and identities for AI systems. From verifiable credentials for delegated authority and portable customer AI ‘memory,’ to digital wallets for AI authentication and ‘proof of human.’

From personal data binding for AI agents and new open protocols for digital trust (not just payments), to new ‘fiduciary AI’ commercial models and zero-knowledge AI auditing so we know what data has been shared by which AI agent, where, why and how.

Woof.

I’ve never been more excited about what’s about to emerge next.

It’s why it’s time for digital trust to be as hyped as AI itself.

TRUSTED AGENTS, EXPERIAN’S AGENT TRUST

Is BankID ready - or able - to adjust to what’s coming?

Apparently there were 1,054,521 bank account ‘switches’ in the UK during 2025. Someone moving their bank account to a new provider.

Hooray for customer empowerment! Hooray for an open market of providers that provide real customer choice!

But hold up.

Retail Banker International has done an analysis of those UK switching stats, and say that only around 2.5% of UK adults switch their primary account each year. You can put the Pom Poms down.

Because it means that 97.5% of people didn’t switch. And more interestingly, means that consumers only switch their bank account every 20+ years.

Let’s take a different view: It means that the banks should know you pretty deeply as a customer.

20 years is a TON of data about your life. Where you live. How much you earn. And in today’s world of digital money, how often you pay for things, where you shop and who you send money to and how often.

It’s why for the longest time, banks have assumed that they should be the logical source of truth for customer identity. ‘Heir apparent’ to the next wave of digital identity.

Two of their better arguments are that banks are regulated, in ways that many of the other identity providers in the market are not, and that consumers mostly trust bank brands over other businesses.

CRIF says that in Europe, 62% of consumers trust their financial services providers. In the US it’s 72%. So, FS providers argue, our banks should become a universal identity provider, right?

Maybe.

Yes, while most people ‘trust’ their bank, the stats for ‘looking after our personal data’ is less good (that’s one for a whole other post). But more importantly, each bank can only reach some parts of the market.

Meaning that each country would need to 1) standardise what ‘Bank ID’ means, 2) build out a banking network where we can rely on any bank’s data to prove who we are.

Which is exactly what’s happened in a range of countries, where BankID is a huge part of the identity market.

But why has it taken off in some places, but not others? It’s because two things must be true.

First, a small number of banks need to cover most of the market. It’s why we see thriving BankID networks in Sweden, Norway, Canada and Belgium. But not in the US or Brazil.

But the second thing that needs to be true, is that those banks need to get on with each other. Which is why it’s taken much longer to agree what BankID looks like in the UK, Germany and Australia.

In each of those counties, a handful of banks enjoy huge market share. But they’ve just not been able to collaborate enough to get something off the ground, even though there have been many, many attempts over the years.

Which brings us to today, and the UK. Where it now looks like the banks have finally got there on BankID, after many years of false starts.

Barclays UK, HSBC, Lloyds Banking Group, Nationwide Building Society, NatWest Group and Santander UK are getting together to develop a financial services-led ‘digital verification service.’

But what interests me most is the timing.

It’s arriving right when digital wallets and portable digital ID are becoming a thing. And from multiple different angles.

At one end of the market, the UK Government is launching digital ID in a ‘GOV.UK Wallet’. At the other, you can see a path for Apple and Google to arrive with a verified ID in their respective wallets. (Yes, they’ll also need to be certified like the rest of the market, just like in the EU, but they are already on the march, and have already activated wallet-based ID in a number of major countries and US states).

It’s about when wallets arrive, not if.

And in the middle of course, there’s everyone else. The UK apparently now has over 200 identity and trust providers, of which only 50 of are certified against the government’s own Trust Framework. That’s one certified provider for every 1M UK adults.

Side question: what’s the collective noun for a group of identity providers… a proof?

So will the UK banks be successful this time? Potentially.

They have the reach, they have the brand awareness, and so-called ‘trust’. But critically, they also have a consumer who’s already comfortable using open banking.

Today, if you need to verify a payment while using a shopping app, you can just jump out of the merchant app experience, approve in your bank app, and bounce back. It’s become a UX familiar pattern.

And that matters A LOT when you are getting customers to change their behaviour.

So I can see UK BankID having some success.

The question is if the ‘bounce out of this app and approve’ flow will become more dominant than an ‘embedded identity’ flow, where the digital ID wallet players can make identity part of the merchant’s own check out.

Like with Apple and Google, and soon the other digital ID wallet players that can embed digital ID within an app.

It’s why I believe ‘Embedded Identity’ will become a whole thing itself, just as ‘embedded finance’ has become. And I wouldn’t bet against the BigTech players if they can get certified in the UK.

Plus, if the UK Government can get its act together on the rollout and comms of the UK digital identity wallet, it would become the highest assurance digital ID in a portable wallet out there, rolled out in parallel to the EU Digital ID Wallet.

So it’s all to play for with the Banks. And for BankID in the UK.

Pay with your bank. Log in with your bank. Now verify yourself with your bank.

Yes, the UK banks involved with BankID already cover most of the UK market. That’s step one done. And they’ve now shown that they can finally get on with each other to make it happen. Step two.

But wait…

What about all the heat and light coming from the AI providers? We are going to need ever-more proof that our AI agents are connected, verified and authorised by a real human.

Most of whom will be verified bank customers.

So can we add BankID to AI flows? Will AI agents be able to connect back to a BankID app to approve Agentic Commerce? Step up to an authentication for a live selfie using my mobile bank app?

And beyond payments, could BankID become a ‘control panel’ for handling AI Agent approvals more generally? Lots to chew on.

It all begs an important new question: is BankID is ready - or indeed able - to adjust to what’s coming?

AI Agents are going to need their own identity and their own money

One of the reasons many people are mis-reading what’s going on with AI agents is that we’re not using the right tools yet.

Today, we’re retrofitting AI agents with yesterday’s infrastructure. For payments, we’re giving agents virtual cards. For identity, we’re connecting them to existing platform accounts. Yes, that gets us part of the way there. But it also creates clumsy experiences, brittle permissions, and a thousand new opportunities for fraud.

So you need to be paying attention to the x402 protocol.

It was baked into the original design of the web, and allows for web-native payments. But it was never activated.

Now HTTP 402 can let services request payment directly inside the web request flow. It’s being governed by the Linux Foundation, and is being backed by the big guns. Coinbase, Cloudflare, Stripe, Visa, Mastercard, American Express, Adyen, Fiserv, Circle, Amazon Web Services, Google, Microsoft, Shopify, Solana and Polygon Labs among many others.

But what about digital identity? It’s an old truth that ‘the internet was born without an identity layer’. It’s why we have such a Frankenstein’s monster of a digital economy today.

Half-living digital identity documents that have been scanned and then tampered with. Uncanny deepfake video streams that pass KYC checks. Creepy sounding voice clones that are like us but not like us.

And why we’re still sending pictures of our identity documents over email.

But now Daniel Buchner and the team at Proof have introduced x401. A path toward web-native identity. Like x402, but where a digital service can ask for a verifiable proof before allowing access.

Not another login button, not another identity workaround, but a native trust layer for the agentic web.

“Today, the mechanisms for presenting identity credentials all assume a person is actively using the UI of a web page or app that requests a credential. AI agents have blown this assumption away.

“Enter x401, a machine-friendly protocol that leverages existing technologies (OIDC4VP, W3C Digital Credentials, and W3C Credential Management) to enable AI agents to detect requests for any form of digital credential (Verifiable Credentials, Passkeys, etc.) and utilize them within the agentic experiences users are relying on more and more every day.

“The internet got its payment layer with x402, but it came thirty years after it was first envisioned.

“Let’s not make the internet wait that long for the HTTP-native identity mechanism it needs in this age of AI.”

Daniel has deep roots in the identity and wallet world. And you should be following this development. Not least because it’s with input from some heavyweights across the AI, wallet and credentials industry, including MATTR, Okta, Circle, Lightspark and OpenAI.

Exciting times.

AI Agents are going to need their own identity and their own money.

Are you ready?

A longer list of things to track…

There are SO many interesting and important Customer Futures things happening at the moment. Here are just a few from my open tabs:

Opinion: The “Transatlantic Data Protection Framework”, covering EU data transfers to the US - is dead READ

News: The UK will now allow digital age checks for alcohol purchases READ

Article: Who Does The Agent Work For READ

Post: You are statistically more likely to survive a plane crash or get into Harvard than to intentionally click on a traditional banner ad READ

Post: The payments industry solved transaction trust years ago… AI is forcing us to solve identity trust next READ

Article: Coinbase is going all-in on the Agentic Economy READ

Opinion: The First Source of Personal Intent READ

And that’s a wrap. Stay tuned for more Customer Futures soon, both here and over at LinkedIn.

And if you’re not yet signed up, why not subscribe: